Double-entry bookkeeping is one of those ideas that sounds intimidating and turns out to be simple. It was written down by a Venetian friar, Luca Pacioli, in 1494 — and it has been the backbone of serious accounting ever since, from medieval merchants to the software running the world’s largest companies. If you have ever wondered what “debit” and “credit” really mean, or why accountants are so obsessed with things “balancing,” this is the plain-English explanation.

Start with the problem it solves

Imagine you track your business with a single list: money in, money out. That is single-entry bookkeeping — basically a chequebook. It is easy, but it is fragile. It tells you your cash went down by $500, but not why, or what you got for it. It has no built-in way to catch a mistake, and it gives you no real picture of what you own and what you owe. The moment your finances get more complex than a personal budget, it stops being enough.

Double-entry fixes this with one deceptively powerful rule: every transaction affects at least two accounts, and is recorded twice — once as a debit and once as a credit — for equal amounts. Money never just “disappears”; it always moves from somewhere to somewhere.

The equation everything rests on

All of accounting balances on one equation:

Assets = Liabilities + Equity

Assets are what the business owns (cash, equipment, money owed to it). Liabilities are what it owes (loans, unpaid bills). Equity is what is left for the owners — the difference between the two. This equation must always hold. Double-entry is simply the mechanism that keeps it true after every single transaction: if one side changes, something else must change to keep both sides equal.

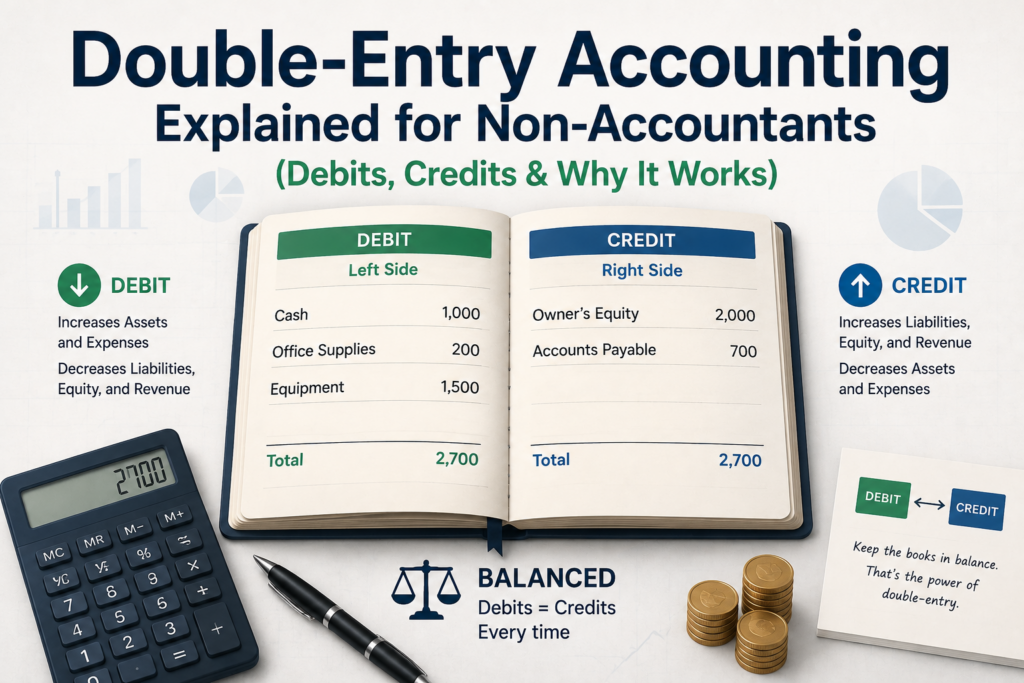

Debits and credits — forget “good” and “bad”

The single biggest source of confusion is assuming debit means “minus” and credit means “plus” (or vice versa). It does not. In accounting, debit just means the left side of an entry and credit means the right side. Whether that increases or decreases an account depends on the type of account:

| Account type | A debit… | A credit… |

|---|---|---|

| Assets (cash, equipment) | increases | decreases |

| Liabilities (loans, payables) | decreases | increases |

| Equity | decreases | increases |

| Income / revenue | decreases | increases |

| Expenses | increases | decreases |

The iron rule that makes it work: for every transaction, total debits must equal total credits. That is what “balancing” means.

Two worked examples

1. You buy a $1,200 laptop with cash. Two accounts move. Your Equipment asset goes up by $1,200 (debit), and your Cash asset goes down by $1,200 (credit). You did not get poorer — you swapped one asset for another. The books balance.

Debit Equipment 1,200

Credit Cash 1,2002. You make a $3,000 sale, paid into your bank. Your Bank asset goes up by $3,000 (debit), and your Sales revenue goes up by $3,000 (credit). Debits equal credits again.

Debit Bank 3,000

Credit Sales 3,000Notice the pattern: you are always answering two questions — what did I receive? and where did it come from? One is the debit, the other the credit.

DailyAccounts — Real Double-Entry Accounting for Your Team

DailyAccounts is a multi-user double-entry accounting system you host yourself. It enforces balanced entries on every voucher — debits must equal credits before you can save — and gives you a chart of accounts, account ledgers with running balances, day book, cash and petty cash books, bank reconciliation, and real-time trial balance, balance sheet and income statement. Browser-based clients over your network, role-based access, no subscription. On the Microsoft Store.

From entries to reports

Individual entries are just the raw material. Their real value is the reports they roll up into — and because everything balances, those reports are trustworthy:

- The chart of accounts is the master list of every account you post to — cash, sales, rent, loans, and so on.

- A ledger gathers every debit and credit for a single account, with a running balance, so you can see the full history of, say, your bank account.

- The day book (journal) is the chronological record of every transaction as it happened — the audit trail.

- The trial balance lists every account’s balance and checks that total debits equal total credits across the whole business. If it does not balance, there is an error to find.

- The balance sheet is a snapshot of the accounting equation at a point in time: assets, liabilities and equity.

- The income statement (profit and loss) shows revenue minus expenses over a period — whether you made money.

Every one of those reports is only possible because each transaction was recorded twice and kept in balance. That is the genius of the system: the structure itself catches errors and produces meaningful financial statements as a byproduct.

Why software makes this painless

Done by hand in paper ledgers, double-entry is meticulous work — every transaction posted twice, every column tallied, every trial balance checked. This is exactly what accounting software exists to automate. A good system enforces the rule for you: it will not let you save a voucher whose debits and credits do not match, so your books literally cannot go out of balance. It posts to the right ledgers automatically and regenerates the trial balance, balance sheet and income statement in real time.

That is the model behind DailyAccounts. You create debit, credit and journal vouchers with separate debit and credit grids, and it refuses to save until they balance — the 500-year-old rule, enforced automatically. From there it maintains your chart of accounts, per-account ledgers with running balances, the day book, cash and petty-cash books and bank reconciliation, and produces the trial balance, balance sheet and income statement on demand. Because it runs as a self-hosted system with browser-based clients over your own network and role-based access, a whole team can post to the same books safely.

Key takeaways

- Double-entry means every transaction is recorded twice — a debit and an equal credit — so money is always traced from one account to another.

- Debit and credit are just “left” and “right,” not “minus” and “plus” — whether they increase or decrease an account depends on the account type.

- Everything serves one equation: Assets = Liabilities + Equity, which must always balance.

- Balanced entries roll up into trustworthy reports: ledgers, trial balance, balance sheet and income statement.

- DailyAccounts enforces balanced double-entry automatically and generates those reports in real time for your whole team.

DailyAccounts — Real Double-Entry Accounting for Your Team

DailyAccounts is a multi-user double-entry accounting system you host yourself. It enforces balanced entries on every voucher — debits must equal credits before you can save — and gives you a chart of accounts, account ledgers with running balances, day book, cash and petty cash books, bank reconciliation, and real-time trial balance, balance sheet and income statement. Browser-based clients over your network, role-based access, no subscription. On the Microsoft Store.

Leave a Reply